Financing India’s Electric Two & Three – Wheeler Fleets

In collaboration with NITI Aayog, the World Economic Forum (WEF) published a report on the financing options in India’s Electric Vehicle (EV) industry. The report highlights capital pools and their lending status in the EV ecosystem, as well as a multi stake holder approach to market de-risking for transitioning two- and three-wheeler fleets to electric.

Two-wheelers (2W) and three-wheelers (3W) account for over 80% of vehicle sales in India.

The adoption of electric 2W (or e-2W) and 3W (or e-3W) has been rising steadily, supported by government policies like Faster Adoption and Manufacturing of Electric Vehicles (FAME), 40+ vehicle manufacturers, others and an impressive cumulative sales of 1 million units has been achieved. However, this is still just 1 million out of India’s total 2W and 3W fleet stock of 250 million – leaving enormous room for continued growth. Achieving 100% electrification of India’s 2W and 3W stock is estimated to require a capital allocation of approximately $285 billion.

Although initial purchase cost of EVs is higher, their running or operational cost is much lower than its counterpart Internal Combustion Engine (ICE) vehicle. Total cost of ownership (TCO) metrics show that they are already ideal for last-mile delivery and ride-hailing fleets, both of which have high daily utilization rates. For instance,

- TCO of e-2W is INR 0.52/km (after accounting FAME incentives and specific Delhi fleet scenario) in comparison to its ICE as INR 2/km

- The TCO of e-3W is INR 1.94/km in comparison to its ICE as INR 2.25/km for the similar scenario of Delhi fleet and accounting FAME incentives

These markets are pioneering the use of e-2Ws and e-3Ws in India and are probably among the first to make the full switch to electric. The ecosystem needs to see a multi-fold increase in capital flow if fleets are to transition quickly. De-risking the market will require improved stake holder collaboration and business model innovation in order to open large capital pools. The different capital pools and their status in EV lending are listed below and divided into three categories.

- Unlocked

- Private equity has been the first pool of capital that has been unlocked and in 2021, the sector received USD 1.8 billion investments by OEMs, fleet owners, fleet operators and infrastructure providers

- Partially Unlocked

- Non-banking Financing Companies (NBFCs) are currently the main source of debt financing in this sector. NBFCs backed by Original Equipment Manufacturers (OEMs) and those specializing in vehicle financing are expected to play a greater role in financing EV fleets.

- Dedicated climate funds like Green Climate Fund(GCF) and Global Environment Facility (GEF) Trust Fund have approved a fund of 1.5 million USD and ~172 million USD. Such funds are being channeled through multilateral banks and other implementation partners.

- Other capital options that are anticipated to encourage and draw investments in green projects in the nation over the coming years include multilateral banks, venture capital, and green bonds.

- Locked

- Most domestic banks and international banks with commercial operations in India have largely stayed away from financing electric two- and three-wheeler commercial fleets.

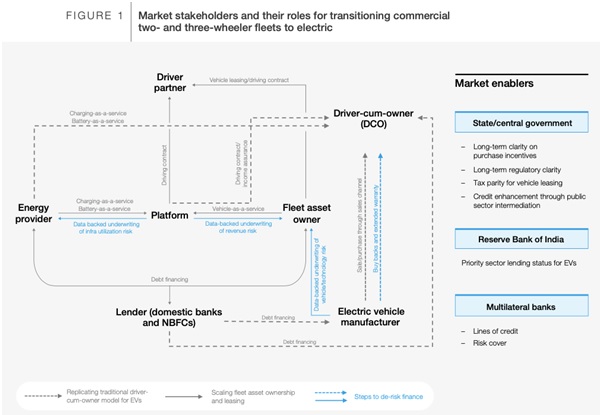

Multi stake holder Approach to Market de-risking

No individual stakeholder can de-risk adoption for e-2W and e-3W fleets. Key stakeholders need to collaboratively engineer and test solutions. Traditionally, the driver-cum-owner (DCO) model has dominated the two- and three-wheeler commercial fleets in India, but DCOs of commercial fleets are not yet comfortable to purchase EVs due to the higher upfront cost of acquisition, lack of confidence in new technology, unassured reliability and unestablished resale value.

- Tripartite agreements to spread the risk

- To de-risk lending and cost of finance for large fleets, a tri-partite lending agreement between lenders, OEMs and fleet asset owners can spread the risk across parties. OEMs can underwrite technology risk, assure buy-back value and ensure after-sales service. Platforms can issue longer-term contracts to driver-partners, aggregators, etc. for deployment of EVs to underwrite risk of insufficient demand – enabling higher asset utilization for vehicle-as-a-service partners – resulting in consistent revenue stream that allows lenders to underwrite EVs for commercial operations and provide low-cost debt-funding to EV fleets.

- Residual value and performance of EVs to be established

- Residual value of EVs is not yet established, which increases uncertainty, affects purchasing decisions, and availability and cost of financing. OEMs can set expectations on residual value of used vehicles through buy-back programmes, or battery and product warrantees. Through use of data and analytics, vehicle manufacturers can track usage-based battery and vehicle health and can make that data available for stakeholders involved in resale.

- Risk underwriting for lending needs to be able to leverage data

- Unlike conventional vehicles, EVs and the supporting charging infrastructure

are in equal part connected devices generating real-time data. These data sets can be leveraged to facilitate data-backed risk underwriting for lending. For example, OEMs can make available anonymous and aggregated data sets on asset utilization and data on health of battery as the vehicle ages. The banks understanding of the technology is limited and provision of these type of insights can introduce competitive financing products.

- Support to vehicle leasing vis-à-vis individual ownership

- India has among the smallest share of 0.8% of leasing-based commercial fleets among large economies. Even as DCOs acquaint themselves with EV, fleet asset owners that rely on vehicle leasing can drive EV adoption in India’s commercial fleets. Leasing of commercial vehicles for fleets has a higher tax burden as compared to individual ownership – parity in tax structures for EVs can help scale up EVs on the road.

- Preferential access to finance is required

- It has been a long-standing demand from the industry that the Reserve Bank of India provide priority sector lending (PSL) status to EVs, on the lines of PSL for renewable energy projects to help channel flow of funds to the sector. Priority sector lending mandates certain banks to direct a specified percentage of credit to priority sectors.

- Government push for setting up of risk-sharing facilities for consumer and fleet finance

- To accelerate the market and steepen the learning curve for lenders, the government can work with multilateral banks and/or deploy its own special purpose vehicle (SPV) to provide sufficient first-loss risk guarantee to lenders. SIDBI-World Bank Electric Vehicles – Risk Sharing Program (EV- RSP) is an example of this.

More details can be referred from the following link: